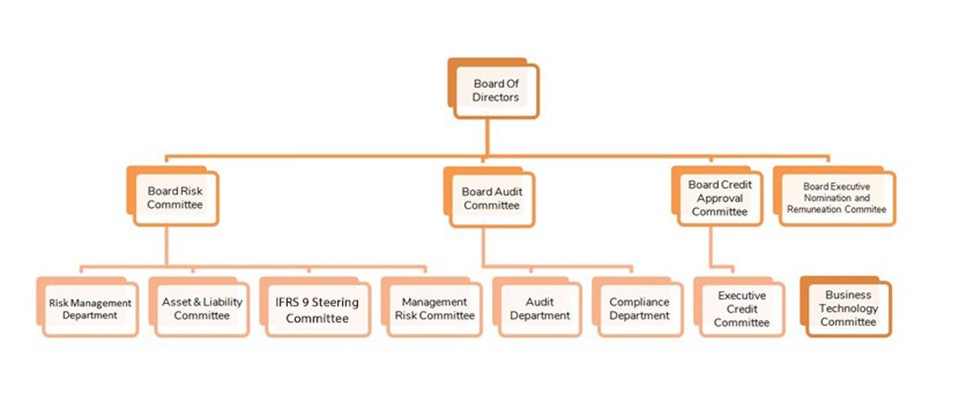

The Bank’s Board of Directors (Board) is the highest governing authority within the Bank structure. Its role is to ensure that the Bank conducts itself in accordance with its core values and develops them further on a continuous and sustainable basis. The Board consists of professionals from various fields and professions and gives representation to the stakeholders & administrators in the process of decision making. The predominance of independent directors has enabled the Board to have meaningful discussions and take an unbiased and qualitative view on matters placed before it. There is a clear segregation between the ownership of the Bank and the management. The roles of the Chairman of the Board and the Chief Executive Officer (CEO) are separated with a clear division of responsibilities at the head of the Bank between the running of the Board and the executive management responsibility for running the Bank’s business. The Board is responsible for overseeing how management serves the long-term interests of shareholders and other key stakeholders.

The Board is the top authority within the Bank and is ultimately accountable to the shareholders. The Board of Directors has established various subcommittees for specific purposes with clearly defined terms of reference and responsibilities. The committees’ mandate is to ensure focused and specialized attention to specific issues related to the Bank’s governance.

Board Level Committees:

The Board is the top authority within the Bank and is ultimately accountable to the shareholders. The Board of Directors has established various subcommittees for specific purposes with clearly defined terms of reference and responsibilities. The committees’ mandate is to ensure focused and specialized attention to specific issues related to the Bank’s governance. Board Audit committee (BAC)

The main functions of the Board Audit Committee are to assess and review the financial reporting systems of the Bank to ensure that the financial statements are correct, sufficient and credible. BAC reviews with the Management the quarterly / annual financial statements before their submission to the Board for adoption. BAC also reviews the adequacy of regulatory compliance, regulatory reporting, internal control systems and structure of Internal Audit and Compliance Departments. BAC also holds discussions with the internal auditors / external auditors on significant finding on the control environment.

The role of Head of Internal Audit is to provide reasonable assurance that the management control framework used within the Bank is operating effectively. The role of Head of Compliance is to ensure that the Bank complies with all the Laws, rules and regulations as applicable under the regulatory framework in Sultanate of Oman and international best practice. Both heads report directly to the BAC.

Board Credit Approval Committee (CAC)

This committee assists the Board to discharge the Board’s responsibilities of oversight and governance in relation to the credit performance of the Bank. The objective of the CAC is to approve large loans falling outside the lending mandate of the CEO and his senior management lending team and optimize the quality and return on deployment of assets.

Board Risk Committee (BRC)

This committee has the responsibility to assist and advise the Board to improve the organizational ability to identify, measure, monitor and control the overall risk profile of the Bank. BRC is responsible for making recommendations to the Board on the risk appetite of the Bank in relation to credit, interest rate, market, liquidity and operational risk with focus on the policy framework. The objective of the BRC is to ensure implementation of risk strategy and policy in addition to ensuring that a robust risk framework is in place within the Bank. BRC will also provide guidance and direction on all credit, market, interest rate, liquidity and operational risks matters. The BRC will ensure that risk management has an institutional framework, independent of business lines, with clear delineation of levels of responsibility for management of risks. It also provides guidance to management level risk committees like Management Risk Committee (MRC), Asset & Liability Committee (ALCO) and Expected Credit Loss Committee (ECL). BRC is a sub-committee of the Board of Directors. It has the responsibility to assist the Board to improve the organizational ability to identify, measure, monitor and control the overall risk profile of the Bank. The committee is responsible for making recommendations to the Board of Directors on the risk appetite of the Bank in relation to credit, interest rate, market, liquidity, operational risk, reputational risk, information security and business continuity management with focus on the policy framework.

The objective of the BRC is to ensure implementation of risk strategy and policy in addition to ensuring that a robust risk framework is in place within the Bank. The committee will also provide guidance and direction on all credit, market, interest rate, liquidity, reputational and operational risk as well as information security and business continuity management matters to ensure that the policy framework is in place. The BRC will ensure that the risk management has an institutional framework, independent of business lines, with clear delineation of levels of responsibility for management of risks. Board Executive Nomination and Remuneration Committee (ENRC)

This committee assists the Board to discharge the Board’s responsibilities of oversight and governance in relation to Human Resources and implementation of the Strategic Plan. Key responsibilities:

Executive Credit Committee (ECC)

The main objective of this Committee is to approve credit and take lending and investing decisions within its delegated authority. CEO is the chairman of the committee. The other members of the committee are CRO (who will sign off only for the level of risk and will not be involved in credit approval decision making as he is a nonvoting member). Head of Corporate Banking, Head of Retail Banking, Head of Operations & CFO. If the CRO does not find the risk to be acceptable, then the proposal will be escalated to Credit Approval committee. All the approvals of the ECC are consolidated and placed to the Credit Approval committee of the Board for noting.

Management Risk Committee (MRC)

A management level committee consists of all divisional heads from Risk, Internal Audit, Wholesale, Retail, Treasury, Operations, HR, IT, Finance, Compliance, Legal. The objectives include (1) To oversee the risk management function of the Bank, (2) To establish improved and enhanced risk awareness and risk culture within the Bank and (3) To minimize the risk losses of the Bank by establishing appropriate process, robust systems, qualified human capital, delegation matrix, segregation of duties, maintain high quality of loan assets, maintain adequate liquidity standards with back up lines, Business Continuity Management preparedness, and excel in customer service.

MRC will be responsible for an overall oversight of the risk management in the Bank. This will broadly include the following responsibilities, though not limited to:

MRC is responsible for managing Operational Risk including the following:

IFRS 9 Steering Committee

IFRS 9 steering committee, a management level committee, is established in response to the governance requirements of IFRS 9 standard. Purpose of this committee is to build a robust framework around the governance of the overall ECL Models and all other such models (as may be prevalent) that may directly/indirectly affect the financial reporting on Expected Loss (EL). The Framework establishes a systematic approach to manage the development, validation, approval, implementation and on-going use of the ECL models. It sets out an effective management structure with clearly defined roles and responsibilities, policies and controls for managing model risk. The Framework is reviewed on a regular basis to ensure it meets regulatory standards and international practices. Any major change to the constitution, framework and/or roles & responsibilities is approved by the BRC.

Asset Liability Management Committee (ALCO)

The Asset and Liability Committee (ALCO) is established under charter of the BRC and is mandated for overall management of the assets and liabilities of the Bank. ALCO manages the Banks’s liquidity, funding, market and capital risks across the organization. ALCO is a strategic decision making committee and although not involved with day to day operating issues, will direct and opine on significant issues impacting the Bank. Policy implementation is delegated to managers who are responsible to the ALCO for achieving stated asset and liability management objectives. Treasury in particular has significant responsibility for executing ALCO decisions in line with ALCO approved policies including the Liquidity Contingency Plan. ALCO is expected to combine the techniques of asset management, liability management, capital management, market risk management into a cohesive process leading to an integrated management of the total balance sheet.

The principle aim of Asset and Liability Management (ALM) is to achieve sustainable and stable profits within a framework of acceptable financial risks, which includes funding and liquidity risk, interest rate risk and foreign exchange risk, equity price risk, trading risk and capital management. ALCO will be the principal management forum for ALM and related longer-term strategy.

BUSINESS TECHNOLOGY COMMITTEE (BTC)

The Business Technology Committee (BTC) is a Management Committee, providing strategic direction and continued advisory services to ensure that the technology environment of the Bank is state-of-art, robust and flexible to meet the challenges faced with changes in the business environment. In this role, the BTC will focus on Business related projects, products and services that require IT systems implementation.